This post is brought to you in paid partnership with QuickBooks

QuickBooks Payments is usually one of the first names that comes up the moment you search for an online payment platform, right alongside Stripe, Square, PayPal, and half a dozen others all promising the same two things: get paid faster, keep more of what you earn. The names are easy to find. What’s harder is knowing which of them actually fits your business, and what you should be checking before you commit to one.

Here’s the short answer. A good online payment platform for a small business comes down to six things: transparent pricing, fast deposit speed, support for multiple payment methods, strong security and compliance, integration with your accounting software, and dependable customer support when something breaks. QuickBooks Payments is built around that exact checklist, combining payment processing with the accounting side of the business so you’re not running two disconnected systems and reconciling them by hand at month end.

The rest of this comes down to why each of those six criteria matters, and what to actually check before committing to a platform.

Transparent pricing

Payment processing pricing is notorious for hidden costs: interchange markups, monthly minimums, PCI compliance fees, early termination fees. The number advertised on the homepage is rarely the number that shows up on the statement. Before signing up for any platform, ask for the full fee schedule in writing, including what happens for card-not-present transactions, refunds, and chargebacks. A platform that publishes flat, per-transaction pricing without a maze of add-on fees is easier to budget around and far less likely to produce an unpleasant surprise three months in.

Deposit speed

How fast money actually lands in the business bank account is one of the most overlooked criteria, and one of the most consequential. Some processors hold funds for two to three business days as standard. Others, including QuickBooks Payments, offer next-day deposit by default. For a business covering payroll, rent, or a supplier invoice on a tight week, that difference of even one or two days can be the gap between meeting an obligation on time and scrambling for a short-term fix.

Support for multiple payment methods

Customers and clients don’t all want to pay the same way. Some prefer a credit card, some prefer ACH bank transfer for larger invoices to avoid card fees, and a growing number expect a digital wallet option like Apple Pay or Google Pay. A platform limited to a single payment type quietly turns away business, or worse, adds friction that delays payment. Look for a platform that supports card, bank transfer, and digital wallets from a single invoice or checkout link, so the customer picks what’s easiest for them.

Security and compliance

Every business accepting card payments needs PCI DSS compliance, and every business handling customer payment data needs to trust that data is encrypted and stored properly. This isn’t optional or a nice-to-have. A platform should handle compliance on the business’s behalf as part of the service, not leave the owner to figure out PCI requirements alone. Fraud protection tools, like automatic flagging of suspicious transactions, are worth checking for as well, particularly for businesses that take a high volume of card-not-present payments online.

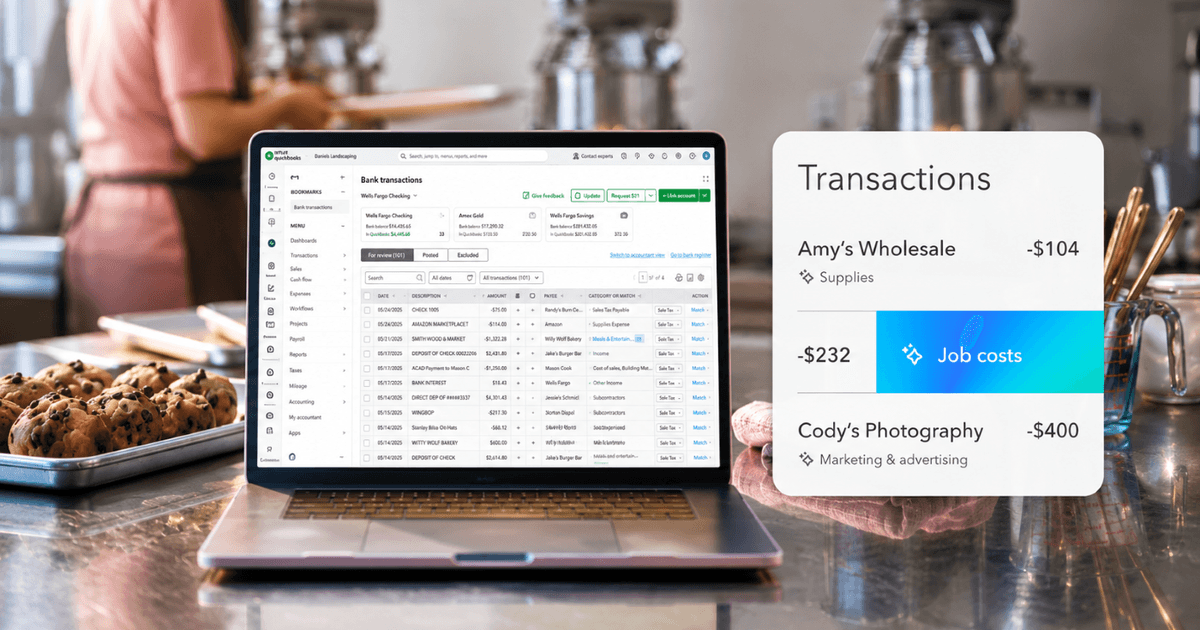

Integration with accounting

This is where a lot of standalone payment processors fall short. If payment data doesn’t flow directly into the business’s bookkeeping, someone has to manually enter every transaction, match it to the right invoice, and reconcile it against the bank statement. That’s hours of admin work every month, and it’s where errors creep in. A platform like QuickBooks Payments records each payment directly against the invoice it belongs to, so the books are accurate in real time without extra data entry.

Customer support

Payment issues tend to happen at the worst possible moment: a declined transaction during a busy sales day, a delayed deposit right before payroll, a customer dispute that needs resolving fast. When that happens, the quality of a provider’s support becomes very real, very quickly. Look for a provider with responsive support through phone or chat, not a ticket queue with a multi-day response time. QuickBooks Payments support sits with the same team that handles the rest of QuickBooks, so a call about a delayed deposit doesn’t start with explaining your entire setup to someone unfamiliar with your account.

What this means for choosing a platform

These six criteria rarely operate in isolation. Low fees paired with slow deposits still leave cash you’ve already earned sitting somewhere out of reach. Fast deposits without accounting integration just move the admin burden from the bank to a spreadsheet at month end. Security tends to go unnoticed entirely, right up until the day it’s missing.

Treat the six as a single package rather than a menu of separate features to compare line by line. QuickBooks Payments was built around that framing, with pricing, deposit speed, payment options, security, accounting integration, and support all sitting under one login instead of six separate vendor relationships to manage. Whichever platform you choose, holding it to the full checklist, not just the fee quoted on the homepage, is what actually protects your cash flow.

This content is paid for by the brands indicated. Digital Trends works closely with advertisers to highlight their products and services to our readers. Although this article is informational and not opinionated, it reflects thorough fact-checking by our team to ensure accuracy. Our dedicated partnerships team, not external advertisers, crafts all branded content in-house. For more information on our approach to branded content, click here.